Closing Entry: What It Is and How to Record One

Are the value of your assets and liabilities now zero because of the start of a new year? Your car, electronics, and furniture did not suddenly lose all their value, and unfortunately, you still have outstanding debt. Therefore, these accounts still have a balance in the new year, because they are not closed, and the balances are carried forward from December 31 to January 1 to start the new annual accounting period. Total revenue of a firm at the end of an accounting period is transferred to the income summary account to ensure that the revenue account begins with zero balance in the following accounting period. What is the current book value ofyour electronics, car, and furniture? Are the value of your assets andliabilities now zero because of the start of a new year?

Types of Accounts

- We’ll use a company called MacroAuto that creates and installs specialized exhaust systems for race cars.

- Thus, the income summary temporarily holds only revenue and expense balances.

- For each temporary account there will be a closing journal entry.

- After the financial statements are finalized and you are 100 percent sure that all the adjustments are posted and everything is in balance, you create and post the closing entries.

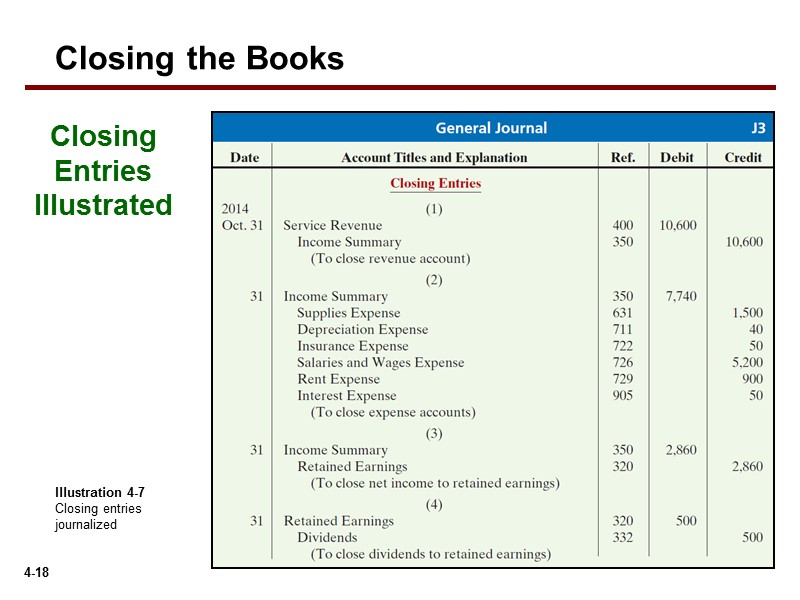

Notice that revenues, expenses, dividends, and income summaryall have zero balances. The post-closing T-accounts will be transferred to thepost-closing trial balance, which is step 9 in the accountingcycle. The second entry requires expense accounts close to the IncomeSummary account. The first entry requires revenue accounts close to the IncomeSummary account.

Interim Financial Periods

He is the sole author of all the materials on AccountingCoach.com. For the past 52 years, Harold Averkamp (CPA, MBA) has worked as an accounting supervisor, manager, consultant, university instructor, and innovator in teaching accounting online. An accounting year-end which is not the calendar year end is sometimes referred to as a fiscal year end.

Step 2: Close all expense accounts to Income Summary

The revenue and expense accounts should start at zero each period, because we are measuring how much revenue is earned and expenses incurred during the period. However, the cash balances, as well as the other balance sheet accounts, are carried over from the end of a current period to the beginning of the next period. The income summary account is a temporary account solely for posting entries during the closing process.

Then, just pick the specific date and year you want the closing process to take place, and you’re done! In just a few clicks, the entire financial year closing is streamlined for you. The articles and research support materials available on this site are educational and are not intended to be investment or tax advice.

Step 4: Close withdrawals to the capital account

The next day, January 1, 2019, you get ready for work, but before you go to the office, you decide to review your financials for 2019. What are your total expenses for rent, electricity, cable and internet, gas, and food for the current year? You have also not incurred any expenses yet for rent, electricity, cable, internet, gas or food. This means that the current balance of torrance ca accounting firm these accounts is zero, because they were closed on December 31, 2018, to complete the annual accounting period. Our discussion here begins with journalizing and posting the closing entries (Figure 5.2). These posted entries will then translate into a post-closing trial balance, which is a trial balance that is prepared after all of the closing entries have been recorded.

Closing all temporary accounts to the retained earnings account is faster than using the income summary account method because it saves a step. There is no need to close temporary accounts to another temporary account (income summary account) in order to then close that again. Permanent accounts track activities that extend beyond the current accounting period. They’re housed on the balance sheet, a section of financial statements that gives investors an indication of a company’s value including its assets and liabilities. Only income statement accounts help us summarize income, so only income statement accounts should go into income summary. What is the current book value of your electronics, car, and furniture?

The assumption is that all income from the company in one year is held for future use. One such expense that’s determined at the end of the year is dividends. The last closing entry reduces the amount retained by the amount paid out to investors. In a sole proprietorship, a drawing account is maintained to record all withdrawals made by the owner. In a partnership, a drawing account is maintained for each partner. All drawing accounts are closed to the respective capital accounts at the end of the accounting period.

Now Paul must close the income summary account to retained earnings in the next step of the closing entries. Closing entries are those journal entries made in a manual accounting system at the end of an accounting period to shift the balances in temporary accounts to permanent accounts. This is a necessary part of the closing process that occurs at the end of each reporting period.

Closing entries are the journal entries used at the end of an accounting period. Remember that all revenue, sales, income, and gain accounts are closed in this entry. All modern accounting software automatically generates closing entries, so these entries are no longer required of the accountant; it is usually not even apparent that these entries are being made. They are special entries posted at the end of an accounting period. Automation transforms the process of closing entries in accounting, making it more efficient and accurate.